Asset Purchase vs. Stock Purchase: Which Fits Your Deal?

When a business changes hands, one early decision shapes almost everything that follows: is the buyer purchasing the company’s assets, or the company’s equity? It sounds technical, but the answer drives who inherits past liabilities, how the deal is taxed, which contracts survive, and how clean the seller’s exit will be. Choosing the wrong structure can quietly cost one side far more than the headline purchase price.

This is one of the most consequential—and most misunderstood—forks in any M&A deal. Here is how the two structures actually differ, why buyers and sellers usually pull in opposite directions, and what to weigh before you commit.

The Two Structures, in Plain Terms

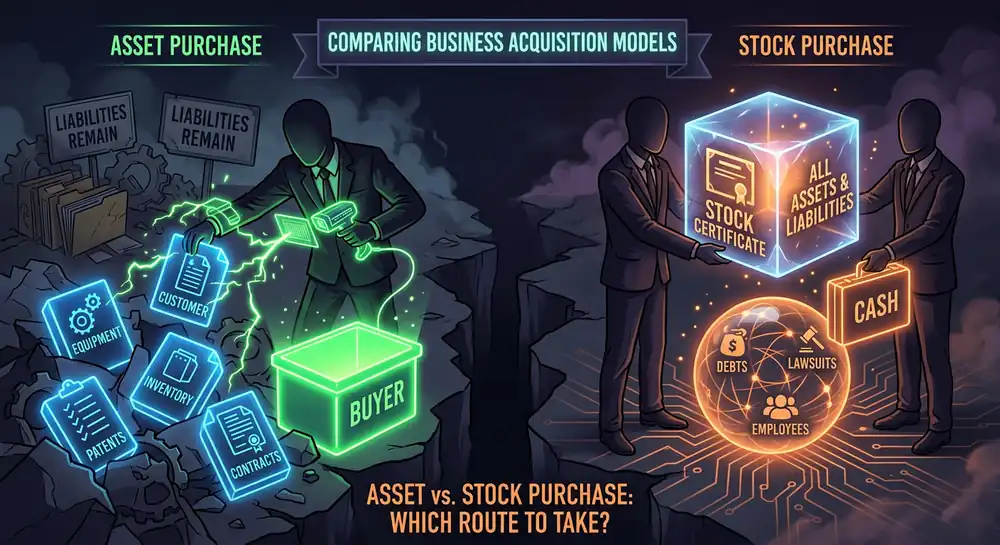

In an asset purchase, the buyer acquires specific things the business owns—equipment, inventory, intellectual property, customer relationships, goodwill—and typically assumes only the liabilities it agrees to take on. The selling entity itself stays with the original owner; what transfers is a defined list of assets and assumed obligations.

In a stock purchase (or, for an LLC, a sale of membership interests), the buyer acquires the ownership of the entity itself. The business generally continues as the same legal entity—often with the same EIN and existing contracts—although banking, signatory authority, lender approvals, and operational details may still need to be updated after closing. Everything the entity owns and owes generally comes along, because nothing technically “moves”; only the owners change.

That single distinction—buying things versus buying the entity that holds the things—is what cascades into every other difference below.

| Issue | Asset Purchase | Stock / Equity Purchase |

|---|---|---|

| What the buyer acquires | Selected assets and assumed liabilities | Ownership interests in the entity |

| Liability profile | Buyer can limit assumed liabilities, subject to exceptions | Entity generally keeps existing liabilities |

| Tax treatment | Often favorable to buyer through basis step-up | Often favorable to seller, depending on entity type |

| Contracts & consents | Assignments and consents often required | Contracts often remain in place, subject to change-of-control clauses |

| Complexity | More transfer mechanics | Often simpler operationally |

A general comparison; outcomes depend on entity type, jurisdiction, and deal-specific facts.

Liability: Who Inherits the Past?

This is usually the buyer’s biggest concern. In a stock purchase, the buyer steps into the entity’s full history. Known and unknown liabilities—an old tax exposure, a lawsuit that hasn’t surfaced yet, an employee claim, a warranty obligation—generally travel with the company. The buyer inherits the good and the bad.

In an asset purchase, the buyer can typically cherry-pick which liabilities to assume and reduce exposure to the rest—though that protection isn’t absolute. Certain liabilities can follow assets regardless of the contract language, including some tax obligations, environmental liabilities, and—under successor liability doctrines that vary by state—sometimes product or employment claims. A structure that looks airtight on paper can still leak if these exceptions aren’t addressed.

Structuring a deal—on either side? The asset-vs-stock decision affects tax, liability, and which contracts survive. It’s worth modeling before the letter of intent is signed, not after.

Book a Free Consultation →Taxes: Where the Two Sides Usually Diverge

Tax treatment is often the reason a deal is structured one way over the other, and it’s where buyer and seller incentives most clearly collide.

Buyers tend to favor an asset purchase because it can deliver a stepped-up basis: the buyer allocates the purchase price across the acquired assets at current value and can depreciate or amortize much of it going forward, reducing future taxable income. Sellers, meanwhile, often prefer an equity sale because it may produce more favorable capital-gain treatment and, in the C corporation context, may avoid the double-tax problem that can arise in an asset sale. But the result depends heavily on entity type, asset mix, purchase-price allocation, depreciation recapture, state taxes, and the seller’s individual tax profile.

The result is a familiar tension: the structure that’s best for the buyer’s tax position is often the worst for the seller’s, and vice versa. This is rarely a stalemate—it’s a negotiation. Price adjustments and allocation agreements can help. In some qualifying transactions, elections such as a Section 338(h)(10) election or a Section 336(e) election may allow the parties to treat an equity sale more like an asset sale for tax purposes, potentially helping bridge the buyer-seller tax gap. The key is that nobody should sign a letter of intent without understanding the after-tax number, not just the gross price. This is general information, not tax advice—the specifics turn on entity type and individual circumstances, and a CPA should run the actual numbers.

Buying or selling a business and weighing asset vs. stock? The structure decides who inherits the liabilities — and the tax bill. Talk through your deal structure →

New laws, before they catch you off guard.

Monthly. New Arizona, California, and Texas business-law changes, the deadlines attached to them, and what they mean in practice. No spam — unsubscribe anytime.

By subscribing you agree to receive emails from Accord & Shield Legal, PLLC. This is general information, not legal advice.

Contracts, Leases, and Consents

Here’s a difference that surprises people. In a stock purchase, the entity keeps its contracts, leases, licenses, and permits, because the entity itself isn’t changing—only its owners are. Most agreements simply continue. The exception is a change-of-control clause, which some contracts contain specifically to give the other party a say when ownership shifts.

In an asset purchase, contracts generally have to be assigned to the buyer, and many cannot be assigned without the other party’s consent. A favorable office lease, a key customer agreement, a software license, a government permit—each may require a separate sign-off to come along. Anti-assignment clauses can slow an asset deal to a crawl or hand counterparties leverage to renegotiate. Identifying which contracts need consent—and starting those conversations early—is often the difference between a deal that closes on time and one that drags.

How the Choice Plays Out in Practice

As a rough generalization: buyers favor asset deals (liability protection, tax step-up) and sellers favor stock deals (simpler exit, better tax treatment). But the default isn’t automatic. Several factors push deals one way or the other:

- Hard-to-transfer assets. If the business runs on permits, licenses, or contracts that are difficult to reassign, a stock deal that keeps them in place can be far cleaner.

- Entity type. S corporations, C corporations, and LLCs each carry different tax consequences, which can make one structure dramatically more attractive than the other.

- Liability profile. When a buyer is worried about unknown past exposure, the protective logic of an asset deal often wins out—backed up by strong representations and indemnities.

- Minority owners. An equity deal may require approval or participation from some or all owners, depending on the entity documents, governing law, drag-along rights, and required approval thresholds—so a holdout can complicate or block it, sometimes nudging the parties toward an asset structure instead.

Whatever the structure, the protections that matter most live in the representations, warranties, and indemnification provisions—the contractual promises about the state of the business and who pays if those promises turn out to be wrong. Structure sets the framework; these clauses allocate the real risk inside it.

The Takeaway

Asset versus stock isn’t a formality to sort out at the closing table. It determines the after-tax economics, the liability you keep or shed, and how much friction stands between signing and closing. The strongest position is to model both structures—ideally with counsel and a CPA working together—before the letter of intent locks in a path that’s hard to reverse.

Our firm advises buyers and sellers across Arizona, California, and Texas on deal structure, due diligence, and the documents that follow. If you’re weighing a sale or acquisition, our M&A practice page covers how we work, and our guide on what a business sale really involves walks through the full arc of a deal.

Frequently Asked Questions

Is an asset sale or stock sale better for the buyer?

Buyers often prefer an asset purchase because it lets them choose which assets and liabilities to take on and may reduce exposure to unknown historical liabilities. Asset deals can also produce a stepped-up tax basis that the buyer may depreciate or amortize over time. The tradeoff is complexity: contracts, leases, licenses, and permits may need to be assigned, reissued, or approved by third parties, and some liabilities can still follow the assets under successor-liability doctrines.

Why do sellers usually prefer a stock sale?

A stock sale is typically simpler and often more tax-favorable for the seller, because the buyer steps into the existing entity and most liabilities transfer with it. The seller usually achieves a cleaner exit with fewer surviving obligations, though strong reps, warranties, and indemnities can shift some of that risk back.

Does the deal structure affect existing contracts and leases?

Yes, significantly. In a stock sale the entity keeps its contracts, so most agreements continue unless they contain a change-of-control clause. In an asset sale, contracts, leases, and licenses generally must be assigned to the buyer, which often requires third-party consent. Anti-assignment clauses can stall or reshape an asset deal.

Can an LLC be sold as a stock sale?

An LLC has membership interests rather than stock, but the same concept applies: the parties can structure the deal as a sale of membership interests (the equity) or as a sale of the LLC’s assets. The equity-vs-asset tradeoffs around liability, tax, and consents are broadly similar to a corporation’s stock-vs-asset choice.

This article is educational and general in nature; it is not legal or tax advice and does not create an attorney-client relationship. Deal structure depends on your specific facts, entity type, asset mix, tax profile, and jurisdiction. Past results do not guarantee future outcomes. Consult a qualified attorney and tax professional before structuring a transaction.

This content is for general informational purposes only and is not legal advice. Reading this page, using this website, or contacting Accord & Shield does not create an attorney-client relationship. Legal advice is provided only after conflicts review and a written engagement agreement.